If BMS and BACS (Building Automation and Control Systems) are doing well, supported by HVAC systems, terminal regulation of transmitters is struggling.

Publi-Information

On April 2, 2026, the ACR – Automation, Climate Engineering and Regulation Union – presented the results of regulation and GTB sales in France in 2025. The ACR, extended to the BACS Alliance, brings together ten manufacturers, i.e. more than 80% of manufacturers of regulation equipment and BMS systems : Belimo, Comap, Danfoss, Distech Controls, resideo (ex-Honeywell), IMI Hydronic Engineering, Kieback&Peter, Siemens, Somfy and Watts Electronics. The BACS Alliance adds acsion energy, Airzone, AQlva Systems, apave, Bureau Vezritas, cameo energy, C4E, CarbOn, Cram energy efficiency, hellio, ecomethods, IMI, Parasitis, Rexel, Sièds Fédérateur d’entreprises, Sensinov, Sobren.

Several big players are missing from these two organizations, including ABB, Legrand and Schneider Electric. But the ACR considers that its figures are reliable and represent the French market.

Yann Plévin, president of the ACR, vice-president of KNX France and, in the civil sector, Head of Standardization and Regulation at Siemens, presented the 2025 results of the French BMS and regulation market. © ACR

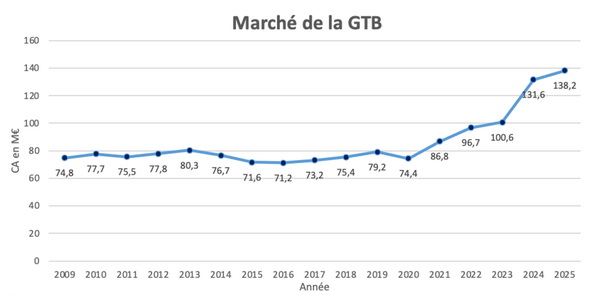

The GTB market. © ACR

GTB grows by 5%

Three relatively clear regulatory texts, the two versions of the BACS decree and the Tertiary eco-Energy Decree impose a timetable for equipping control solutions and drive the market. According to the ACR, however, “investments focus on the regulation of HVAC (Heating, Ventilation, Air Conditioning) systems, with particular attention to the hydraulic balancing of installations“. Most of the activity on the GTB market, adds the ACR, is driven by regulatory compliance operations with a priority given to HVAC which consists of updating existing installations with new standard solutions.

The ACR also recalls that it is essential to implement BACS with open standardized protocolssuch as BACnet, KNX, etc., to comply with the interoperability requirement contained in the BACS decree and to facilitate a gradual upgrade of installations to class A or B BMS systems while controlling costs.

Multi-discipline processing units (-70%), which allow lighting and blinds to be addressed in addition to HVAC, are falling sharply. © PP

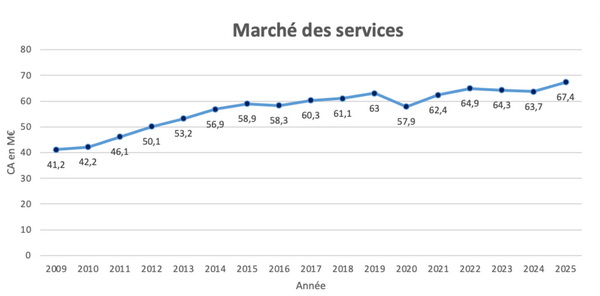

The service market around GTB returns to growth at 5.8% in 2025, to stand at 67.4 million euros. What the ACR calls “services” are technical assistance, training, the supply of spare equipment, troubleshooting, and even maintenance contracts. © ACR

As demand mainly relates to an update of existing installations in 2025, customers are naturally turning to BACS manufacturers for the upgrade of existing installations. And, strongly emphasizes the ACR, commissioning and preventive maintenance operations must contribute to reducing the gap that may exist between the design, installation and operation of “BMS systems and regulation” efficient.

For the future, the ACR further indicates, the technological challenge will be the integration of cybersecurity requirements in the building, of which BACS constitute a central link. Manufacturers have well anticipated these new future constraints and are already offering equipment implementing cybersecurity standards such as BACnet/SC and KNX Secure. By 2030, once buildings are equipped with BACS corresponding to the regulatory requirement which will become a sort of de facto minimum, “the market could focus on the deployment of instruments to measure real energy consumption” hopes the ACR.

Regulation progresses by 1.9%

According to the ACR, the hot water loop is more resistant to the fall in new construction with 2.9% growth in 2025. Distribution regulation devices, which make it possible to improve hydraulic balancing functions, are making particular progress. THE deadlines of the “Regulation” Decree (Decree No. 2023-444 of June 7, 2023), also known as the thermostat decree, and its complement, the decree of June 8, 2023, have been postponed to 2030, the level of requirements is known. This concerns collective and tertiary housing, heating and cooling and requires that:

– the local control system of a heating installation automatically regulates, according to a minimum hourly step, the heating temperature per room or, if justified, per heating zone;

– The system allows manual control and programming of the interior target temperature according to, at least, the following four stages: “comfort”, “reduced”, with automatic switching between these two stages, “frost protection”, “off”;

– The system allows automatic or manual switching between all of these speeds;

– Finally, central water heating systems are equipped with a regulator falling into one of classes IV, V, VI, VII or VIII, as defined in paragraph 6.1 of Commission Communication 2014/C 207/02 within the framework of Regulation (EU) 813/2013 of the European Commission.

We understood, and many manufacturers with us, that simple thermostatic valves were no longer suitable. The ACR is not sure of this and is requesting regulatory clarification on this point. Especially since thermostatic faucets still make up the majority of sales of terminal heating regulation and are falling less (- 3.4%) than communicating solutions (- 7.7%), in other words motorized faucets connected by an open protocol to a centralized thermostat. © PP

The ACR considers that these communicating solutions, allowing time programming in each room, exceed the regulatory requirement. They are always covered by a standardized operation giving right to CEE according to the BAR-TH-173 sheet. Programmable room thermostats (+ 3.5%) continue to gradually replace non-programmable models.

Solutions for regulating energy distribution, indicates the ACR, are those which have been the most popular regardless of the size and nature of the buildings concerned. Dynamic balancing solutions are more than ever recognized as essential to achieve performance and comfort objectives. The ACR therefore notes a 5.7% increase in PICV valves or pressure-independent automatic regulation and balancing valves, and a good 35% in 0-10V motorized valve actuators.

The ventilation and air conditioning regulation market remains at a level equivalent to 2024 (+ 0.8%). Here, regulators for communicating HVAC terminals experience varying trends depending on the protocols and decrease slightly in total (- 0.4%). Unsurprisingly, proprietary protocols have almost disappeared now. © PP