The energy transition leads to a reduction in fossil fuel consumption, and therefore a reduction in energy tax revenue. This reduction will have to be compensated for by an increase in taxation.

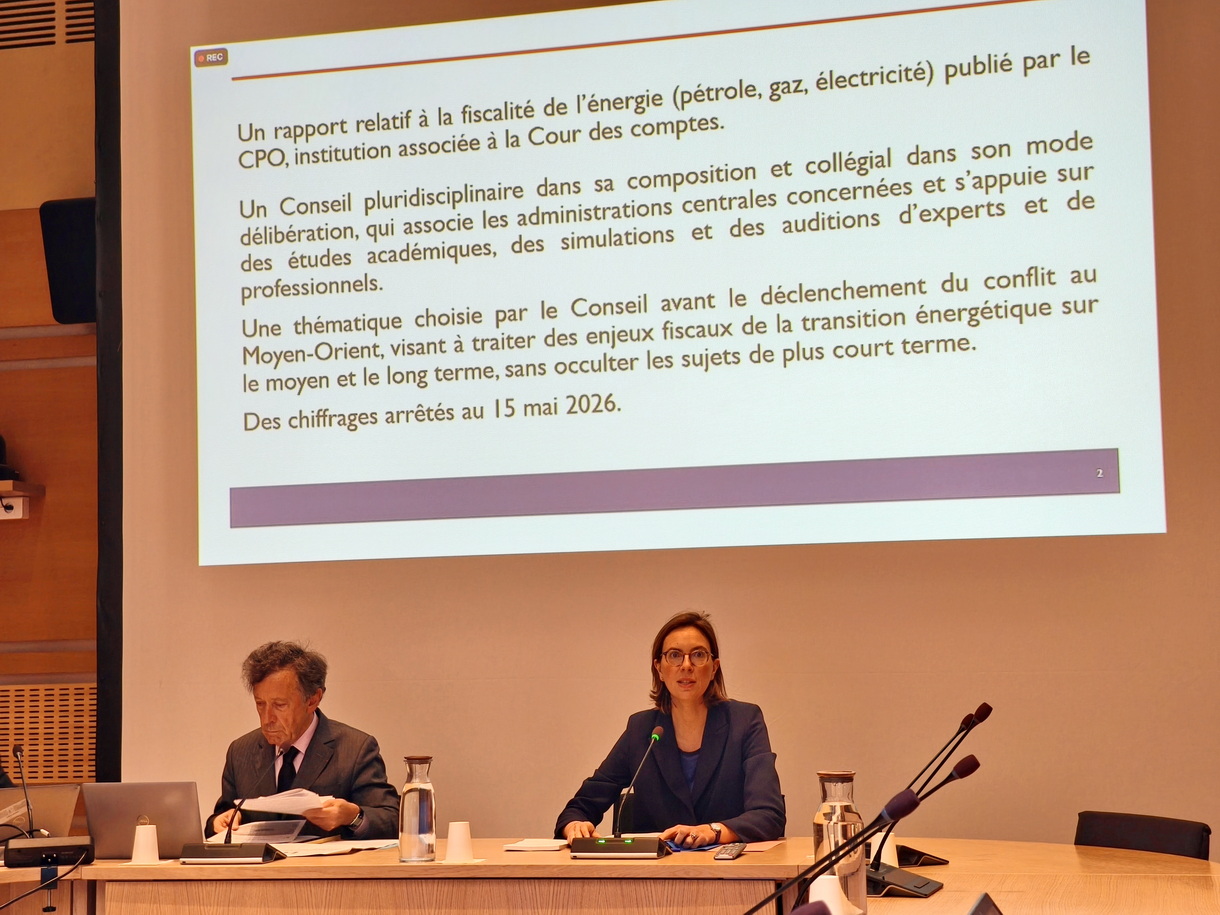

On June 3, Amélie de Montachalin, who chairs the Court of Auditors, presented the report from the Council for Compulsory Deductions (CPO) on energy taxation. Created in 2005, the CPO is a body associated with the Court of Auditorss. He is “responsible for assessing the evolution and economic, social and budgetary impact of all compulsory levies, as well as making recommendations on any question relating to compulsory leviess”: taxes, duties and social security contributions.

At the beginning of June, the CPO has published a report entitled “What future for Energy taxation?”

The structure of energy taxation is complex

There energy taxation brought in €59.7 billion in 2024, or around 2% of Gross Domestic Product (GDP) that year. Essentially, this income is based on VAT on energy products (€17.6 billion in 2024) and on excise on energy products (€39.5 billion). The excise is an indirect tax levied in particular on the consumption of energy products, but also on energy-intensive vehicles, on air conditioners for automobiles, etc.

There energy taxation in France is notably codified by two European directives:

–2020/262 of December 19, 2019 on excise duties;

–and 2003/96/EC of October 27, 2003 on energy taxation.

Unfortunately, these two directives provide for possibilities for exemption and rate reductions, which successive French governments have made extensive use of: in 2024, 35 derogation schemes have been identified in France, at a cost of €15 billion for public finances. These tax advantages concern in particular transport, agriculture, fishing, industry, construction and public works, as well as various products, including non-road diesel, biofuels, biomass valorization installations, biogas injected into the network.

The European emissions trading system

To complicate the matter, theEurope has adopted the ETS (European Emissions Trading System)), also known as ETS (Emissions Trading Scheme) to reduce its Greenhouse Gas (GHG) emissions. The first period of the ETS, in force since 2005, covers large industrial installations, electricity production and part of aviation, i.e. around 40% of European emissions and almost 20% of French emissions.

THE EU ETS 2 (ETS 2), adopted in 2023 by the European Unione, is a new carbon market which will start in 2028 and which will cover GHG emissions from fossil fuels used in the road transport, building, construction and small industry sectors. At the same time, the price of carbon is increasing and free allowances are gradually disappearing. This means, for example, that heating with oil or gas will cost more from 2018. The mechanism is not yet very clear, but we will present it to you in detail as soon as we understand it.

Having said this, the CPO decided toanalyze the implications of energy taxation within the framework of the third version of the National Low Carbon Strategy (SNBC 3)put out for consultation in December 2025, but not yet approved.

In the short term, changing energy taxes is a bad instrument

Faced with the rapid increase in oil prices, the CPO believes that energy taxation is poorly suited to supporting a price smoothing function in the short term and recommends not using it for compensate for the increase in the price of fossil fuels. Indeed, he underlines, the VAT product increases with the increase in energy prices, but the excise product decreases, which is based on the quantities sold, decreases with inflation which leads to a reduction in consumption. The CPO estimates that if prices remained at their mid-May level and consumers reduced their demand in the same way as during the previous oil shock of 2022 (war in Ukraine with sharp increase in gas prices), the increase in VAT and the reduction in excise duty would lead to an overall increase in the proceeds from taxes on fossil fuels of only €0.2 billion in a full year. Which on a country scale is not much. The devil is in the details however and some businesses are affected significantly more than others. The CPO considers that cash flow aid or highly targeted and reversible budgetary measures to support the income of businesses and professionals most exposed to the oil shock would be more effective for affected businesses and less costly for public finances than a general reduction in VAT.

The energy transition will reduce energy tax revenue

In the longer term, but from 2030, for example, the energy transition will lead to a significant drop in fossil fuel consumption, in favor of electricity. What mechanically goes reduce energy tax revenue. The CPO, citing the General Directorate of the Treasury, believes that the net energy excise revenue should fall by €15 to €30 billion. And, adds the CPO, new revenues from carbon markets and SEQE and SEQE-2 mechanisms will not compensate for these losses. The CPO therefore recommends raising the reduced rates to the levels indicated by European directives, and revising the excise to align the taxation of diesel with that of gasoline. Then, he suggests promote the energy transition by increasing taxes on fossil fuels and by reducing those supported by electricity.

At the same time, the CPO recommends supporting the implementation of the new SEQ-2 carbon market with investment aid to reduce dependence on fossil fuels. Let’s think, for example, of support for the installation of high-power heat pumps in the collective and tertiary sectors. But, underlines the CPO, these added mechanisms will lead to a drop in revenue for public finances, which will have to be compensated by a reduction in spending – never seen before – or by an increase in revenue through taxes on the use of energy – electricity – or on other products whose consumption is not very elastic in relation to changes in prices. The CPO recommends a “explicit and early arbitration” to create a predictable framework for households and businesses.